Loan issues

Conflicts and issues in the microcredit market.

_420x760_78c.jpg)

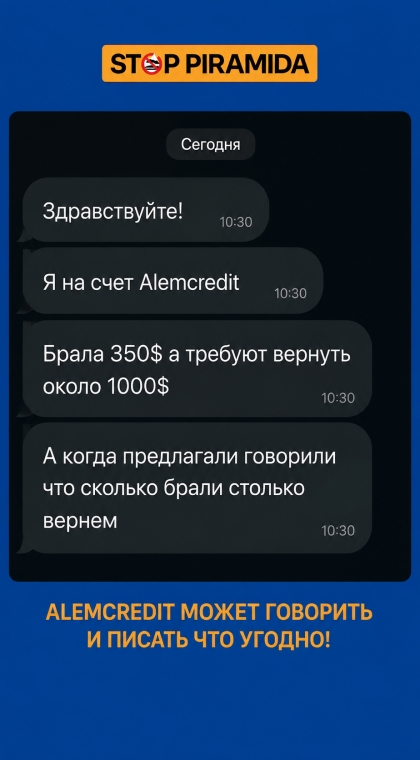

The Stop-Piramida.kz project continues to receive reports from users of the Alem Credit platform. People report psychological pressure, calls to their relatives, sharp increases in the amount claimed as debt, and other actions that raise concerns among borrowers.

We recommend staying calm, not giving in to psychological pressure, and not trusting promises to "freeze," "write off," or significantly reduce your outstanding debt.

If you have encountered a similar situation, contact Stop-Piramida.kz for a free consultation. We also provide report templates for submitting complaints to government authorities.

We continue warning people who use the services of the “Alem Credit” lending platform.

In this episode, we examine a case in which a borrower's bank accounts were blocked by the Anti-Fraud Center shortly after receiving a loan. The reason was that the loan funds had been fraudulently withdrawn from another person's bank card.

As a result, a borrower may unknowingly become involved in a fraudulent scheme, face bank account restrictions, and be subjected to checks by law enforcement authorities.

We also draw attention to the fact that the website of the platform displays the details of virtual international payment cards issued by an AIFC resident, which are used as money mule cards.

How does the illegal lender "Alem Credit" profit from borrowers?

The platform charges a 5.86% daily penalty for overdue payments, while the National Bank of Kazakhstan sets the limit for penalties at no more than 0.3% per day.

This illegal platform exceeds the official threshold by almost 20 times.

Over 700 BILLION% APR (annual percentage rate)?!

How much does the illegal platform "Alem Credit" make from borrowers?

"Alem Credit" and your government ID photo: what's the connection?

"Alem Credit" doesn't just inflate borrowers' debts up to six times — the platform is also suspected of unlawfully using personal data.

How did illegal lenders obtain borrowers' relatives' contact details and passport-style photos submitted through Public Service Centers?

"Alem Credit" is back in the spotlight. Using aggressive advertising across social media and even taxi aggregator platforms, the company continues to rapidly increase its traffic. In May 2026 alone, the "Alem Credit" website recorded 138,000 visits.

At the same time, we continue to receive complaints about the company's activities from people across Kazakhstan.

Starting in 2026, microfinance organizations (MFOs) in Kazakhstan will be subject to additional borrower assessment requirements. Before issuing a microloan, lenders will be required to evaluate a client's ability to repay, credit history, debt burden, and potential fraud indicators.

Representatives of government agencies, including the Agency for Regulation and Development of the Financial Market, the Agency for Financial Monitoring and the Prosecutor General’s Office, took part in the meeting. Following the discussion, the relevant authorities were instructed to promptly review the situation. Citizens were also warned not to transfer funds to third-party bank cards listed as loan repayment details on the "Alem Credit" platform.

The Agency of the Republic of Kazakhstan for Regulation and Development of the Financial Market is developing a digital platform that will allow borrowers to settle unsecured loan and microloan debts online.